KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance are crucial for businesses to ensure they are not facilitating illegal activities such as money laundering, terrorist financing, or other financial crimes.

This blog post explores the fundamental concepts of KYC and AML and how remote KYC can provide a seamless customer experience, help your business comply with regulatory requirements, and even increase the security of your business and your customers.

What is AML?

Anti-Money Laundering (AML) is a set of laws, regulations, and procedures designed to prevent individuals and organizations from disguising the proceeds of illegal activity as legitimate funds.

AML aims to detect and prevent money laundering, terrorist financing, and other financial crimes. Financial institutions and other regulated entities such as banks, money service businesses, and casinos are required to implement AML programs for continuous risk assessment to detect and report suspicious activity to the relevant authorities.

AML compliance programs typically involve the following elements:

- Customer due diligence (CDD) and know your customer procedures

- Ongoing monitoring of transactions and account activity for suspicious behavior

- Reporting suspicious activity to relevant authorities

- Record-keeping and reporting requirements

Compliance with AML regulations is essential for financial institutions and other regulated entities to avoid financial penalties, legal liabilities, and reputational risks.

What is KYC?

Know Your Customer (KYC) refers to the process of verifying the identity and other personal information of customers or clients. KYC is a regulatory requirement in many countries, particularly in the financial sector, where financial institutions such as banks and other financial service providers are required to obtain and verify the identity of their customers.

KYC requirements typically involve collecting personal information such as name, address, date of birth, and customer identification documents such as a passport or driver’s license. This information is then verified against reliable and independent sources, such as government databases, to confirm the customer’s identity.

High-risk customers undergo enhanced due diligence (EDD) as part of the KYC process. Companies establish protocols for managing these customers and typically implement more rigorous monitoring measures to track their financial activity.

KYC is essential for preventing fraud, money laundering, and other financial crimes. It helps financial institutions identify and mitigate risks associated with their customers, and it also helps them comply with regulatory requirements.

What Are the Challenges Related to KYC and AML Compliance?

Traditional KYC processes can be complex, time-consuming, and expensive. Organizations operating globally face challenges due to varying government and regulatory requirements across countries and regions. In 2023, global financial institutions faced a total of $6.6 billion in penalties for failing to comply with anti-money laundering (AML), KYC, and other regulations. This is a 57% increase from 2022, when the total was $4.2 billion.

In addition, other common challenges are:

- Frustrating Customer Onboarding: Businesses must verify the identity of their customers before offering them services or products. This process can be time-consuming and may lead to customer frustration or abandonment if not done in a timely manner.

- Repeat Customers Subject to Repeat Frustration: When repeat customers attempt to open multiple accounts, businesses require loyal customers to go through KYC again. Instead of rewarding loyalty with a smoother experience, customers are met with the same friction as new customers.

- Data Management: Businesses need to collect, store, and manage a significant amount of customer data to comply with KYC and AML regulations. This can be challenging, especially if data is stored in different systems or if data quality is poor.

- False Positives: AML compliance requires businesses to screen transactions and customers for potential risks. This can result in a large number of false positives, which require additional investigation and can slow down transaction processing.

How does Trust Stamp Facilitate KYC and AML Compliance?

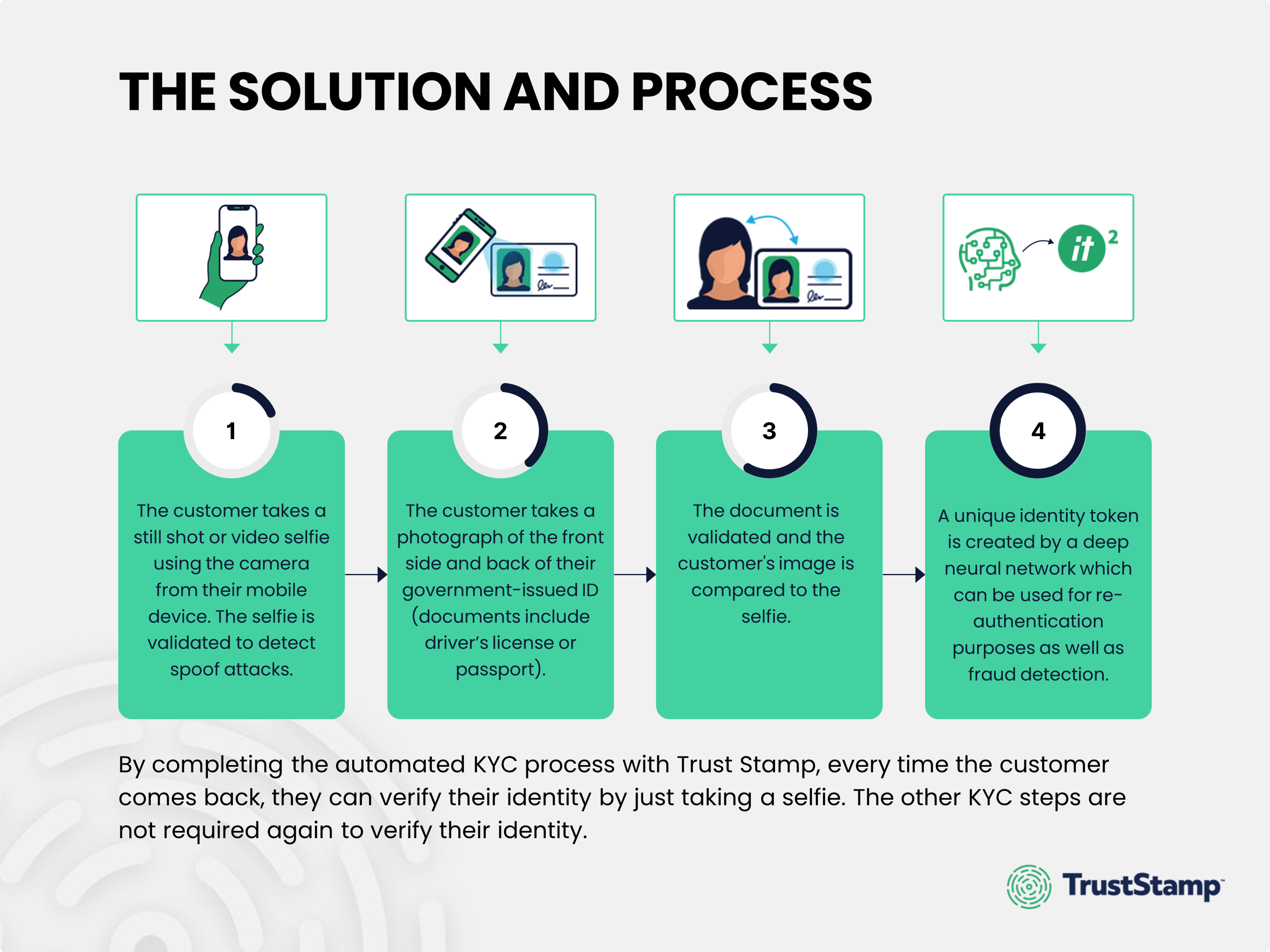

To address the growth of remote and digital experiences for clients and along with the increase in KYC/AML requirements, Trust Stamp empowers businesses with remote and automated KYC solutions. Using document scanning and facial recognition through a standard smartphone camera, consumers can complete a KYC process quickly and easily.

Our multi-layer and automated process speeds up the KYC process for institutions and customers. It utilizes machine learning to identify risky transactions and potential non-compliance.

Advantages of Remote KYC for KYC and AML Compliance

- Reduces Friction During Customer Onboarding – During the customer onboarding process, incorporating Trust Stamp’s KYC reduces friction by eliminating the need for manual identity checks and the submission of physical documents. Trust Stamp’s automated KYC supports the account opening of users by comparing their faces with the photo on a government-issued ID card captured using a smartphone camera. This results in a quicker and more convenient process for the customer, as they only need to take a photo of their face to complete the authentication process.

- Accurate Face Match and Liveness Verification – Trust Stamp’s Facial biometrics ensure accurate ongoing verification by Trust Stamp’s proprietary face match and liveness algorithms. This provides secure verification as only the account holder can access their account. Ongoing authentication ensures accurate ongoing verification.

- Enables Quick and Seamless Transactions – Trust Stamp’s Facial biometric authentication streamlines online transactions by quickly and accurately verifying account holders’ identities anywhere with a secure selfie. The selfie image is transformed into a privacy-preserving identity token. Once created, this token can be used to enable any subsequent identity verification for quick and seamless transactions.

Streamline KYC Onboarding with Trust Stamp

Get in touch with Trust Stamp’s KYC and AML compliance experts to learn more about how you can fulfill your compliance duties while providing a seamless customer experience.